Still, middle market firms are expanding, albeit at a slower rate when it comes to employment, business capital spending and inventory accumulation. Firms may be somewhat underestimating the economic impact of a potential vaccine and what the economic landscape will look like in the second half of 2021.

We strongly suspect that the unlocking of economic activity—20% of a $20 trillion economy—will stimulate the economy in such a fashion that risks around the policy outlook will be a second order affair in contrast to what we expect will be a 3.5% pace of growth next year. We anticipate that as the timetables on the distribution of a safe and effective vaccine become public knowledge, middle market business sentiment will improve and expectations will become aligned with our bullish outlook.

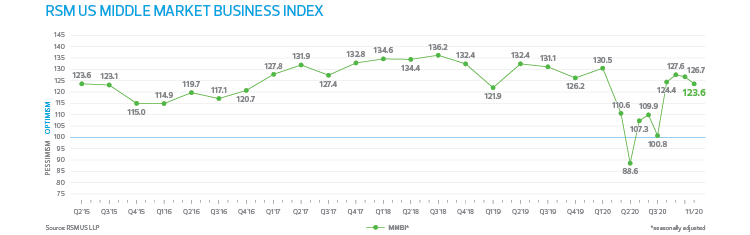

Expectations decline

Survey responses to the questions that make up the index were mostly lower in November, with a notably sharp reduction in the share of respondents—49%, down from 66%—expecting the U.S. economy to improve over the next six months, as well as a plurality stating that conditions had improved.

While the magnitude of the drop is noteworthy, the direction of the change is not surprising given the expectation that the recent resurgence of COVID-19 will weigh on the economy in the fourth quarter with the effects of the virus now starting to show up in several important indicators. The change in November in both the seasonally adjusted and nonseasonally adjusted indices are statistically significant at levels of 0.05 and .10.

The weakening in the forward-looking questions of the RSM US MMBI is consistent with the view that the negative effects of the virus will intensify heading into the winter.

The monthly figures on employment illustrate a significant slowing in job growth in the first two months of the fourth quarter, which almost certainly reflects the deceleration in the domestic economy amid the pullback from the public and the increase in local lockdowns. Survey data point to general restraint on hiring and compensation among middle market firms currently and going forward.

While a majority of firms are willing to increase compensation to attract and retain talent, there is some hesitation among firms on what the post-pandemic economy will look like and how the era of technology, telework and automation will shape the middle market in the years ahead. Only 40% of firms said they had increased capital expenditures, or outlays on productivity-enhancing equipment, software and intellectual property, and 49% indicated that they intend to do so over the next six months. From our perspective, this is going to be one of the major constraints faced by middle market firms as technological change is pulled forward, reshaping the economy and the middle market.

The share of middle market executives reporting higher revenues and profits was roughly the same as in the past couple of months, with a majority of respondents indicating that they anticipate solid growth.

Little evidence of disinflation

While the pandemic-induced shock to the economy has unleashed modest disinflation across the country, there is little evidence of a disinflationary impulse in the middle market. The same share of respondents reported higher selling prices in November as in October, while more firms raised worker compensation. The latter highlights the K-shaped nature of the recovery with limited slack in better-paying industries such as health care, where staffing needs are rising, and business and professional services, where employees can perform their work from home in most cases. However, the surplus of workers who previously worked in the damaged services sector implies that wage pressures are likely not to be an issue in the food and beverage, retail, or leisure and hospitality industries next year.

Fewer firms reported that credit was easier to obtain, consistent with tighter lending standards, and slightly more firms plan to borrow, presumably to take advantage of low interest rates.

While the late-year weakening in the economy tied to the spread of COVID-19 could prove to be substantial, by most accounts the economy had already begun to slow through October before new virus cases started to pick up and restrictions on activity started to be more meaningful. The lagging indicators released in recent weeks show strength in construction spending, as well as orders and shipments for core capital goods, signaling a solid start to the quarter for fixed business investment. Meanwhile, the widening in the trade deficit in October masked solid gains in both exports and imports that point to firming economic activity domestically and abroad.

Virus-related developments, slower job market improvement and fading federal fiscal stimulus appear to be weighing on consumer spending, however, suggesting a rough start for holiday spending. Though government figures on spending show that consumption continued to recover at a solid rate through October, the same data show a drop in personal income with lower transfer payments easily offsetting an increase in employee compensation. With consumption up and income down, the savings rate is falling but to a still-elevated double-digit rate that should fall as consumption picks up over time once vaccine distribution begins.