CFCs in financial distress

Creditor Considerations

Worthless stock deduction

Section 165(g) generally provides that if a security (including a share of stock in corporation) becomes worthless during a taxable year – such loss shall be treated as a loss from the sale or exchange, on the last taxable day of the year. Section 165(b) states that the basis for determining the amount of the deduction for any loss shall be the adjusted basis provided in section 1011 for determining the loss from the sale or other disposition of property.

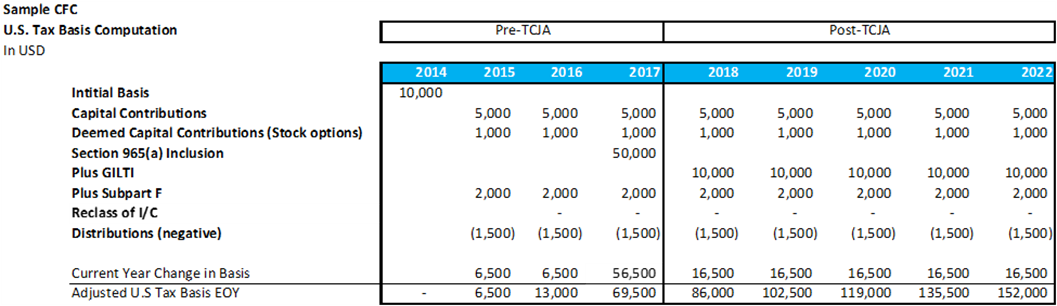

For example, assume a U.S. shareholder owns shares in a CFC with an adjusted basis of $100 and the CFC become wholly worthless during the year. The U.S. shareholder would thus be entitled to a $100 capital loss.

Section 165(g)(3) provides an exception to capital loss treatment by allowing a domestic corporation an ordinary loss on the disposition of an affiliated corporation. To qualify as an affiliated corporation, the U.S. corporation must directly own 80% of the vote and 80% of the value of the subsidiary.[15],[16]

In addition, section 165(g)(3) generally requires that more than 90% of the aggregate of the subsidiary’s gross receipts for all taxable years have been from sources other than royalties, rents, dividends, interest, annuities and gains from sales or exchanges of stocks and securities.

As such, if a controlled foreign corporation (CFC) becomes wholly worthless, the U.S. shareholder can claim a capital loss deduction equal to its adjusted basis in the stock of the CFC under section 165(g). However, if the requirements of section 165(g)(3) are met, they can instead claim an ordinary loss. Based on the previous example, if the requirements of section 165(g)(3) are met, the U.S. shareholder would have a $100 ordinary deduction (rather than capital loss).

As section 165(g)(3) requires direct ownership, the provision is not available if the worthless stock deduction was not taken with respect to a first-tier CFC. Alternatively, if a solvent intermediary CFC could be liquidated – then section 165(g)(3) treatment might be available. However, the transaction would also subject to the Treas. Reg. section 1.165-5(d)(2)(ii) anti-abuse rules.[17]

Bad Debt Deduction

Section 166(a)(1) allows for a deduction for any debt that becomes wholly worthless during the year. The amount deductible equals the adjusted basis of the debt.[18] Under certain circumstances, section 166(a)(2) provides for partially worthless debt deductions.

For example, assume a CFC owes its U.S. shareholder debt with an adjusted basis of $100. It is determined that the debt has become wholly worthless in 2024. As such, the U.S. shareholder can take a $100 bad debt deduction.

Debtor CFC Considerations

Cancellation of Debt Income

While the shareholder creditor may take a bad debt deduction or worthless stock deduction, the debtor generally would have correlative cancellation of debt income (“CODI”). Section 61(a)(11) provides that CODI is included in taxable income. For example, assume a corporation borrows $100 from a creditor. The corporation increases an asset (cash) and has a corresponding increase to its liabilities (note payable). If the creditor forgives $100 of the loan,[19] then the corporation has been relieved of $100 of liabilities, and thus would reflect $100 of CODI.

Since CODI is included in taxable income[20] and CFCs are treated as domestic corporations for purposes of calculating gross income under Treas. Reg. section 1.952-2(a)(1), taxable CODI is likely includable in the calculation of GILTI as section 951A(c)(2)(A) tested income. However, to the extent available,[21] the section 250 deduction could offset up to 50% of such GILTI income.

There are two important exceptions to this rule. To the extent the debtor is insolvent, section 108(a)(1)(B) provides that such CODI is excluded by the amount of insolvency immediately before the debt discharge. In the prior example, if the debtor is insolvent by $40 immediately before the debt discharge, $40 of the CODI would be excluded from taxable income (and $60 would be taxable to the debtor).[22]

Another prominent exclusion is the bankruptcy exclusion, in which CODI is excluded if the discharge occurs in a “title 11 case.”[23] The term “title 11 case” means a case under the Bankruptcy Code[24] if the taxpayer is under the jurisdiction of the court; and the discharge of indebtedness is granted by the court or pursuant to a plan approved by the court.[25] Where a debt cancellation occurs during the bankruptcy process, but not pursuant to a plan approved/granted by the court, the bankruptcy exclusion does not apply.[26] If the debt discharge occurs pursuant to a plan approved by the court, the level of insolvency of the debtor is irrelevant to the amount of the exclusion. In other words, the burden of proof is on the taxpayer to establish the amount of insolvency outside of a title 11 bankruptcy case.[27] One benefit of a title 11 bankruptcy filing is the absence of the requirement for the taxpayer to establish the amount of insolvency.

Generally, where an exclusion (i.e., bankruptcy or insolvency) applies, a tax attribute reduction is required under Section 108(b), which provides mechanical ordering rules. The mechanics of the attribute reduction resulting from excluded CODI is beyond the scope of this article; however, while not entirely clear, it appears logical that tax basis in assets of a CFC would be reduced to the extent that CODI is excluded due to insolvency or U.S. title 11 bankruptcy.[28]

Attribute reduction generally has the effect of providing the debtor with a “fresh start” – such that the CODI is excluded from taxable income (due to insolvency or bankruptcy) after the determination of tax for the year in which debt is cancelled.[29] The cost of reducing attributes is that future income and taxes would likely be increased. For a CFC, the loss of basis in assets would have the effect of reducing depreciation deductions, which would have the effect of increasing tested income and thus the GILTI inclusion to the U.S. shareholder.

Revenue Ruling 2003-125

Revenue Ruling 2003-125[30] clarifies the tax consequences when a U.S. shareholder converts a CFC to a disregarded entity. Specifically, the ruling addresses the conditions under which a shareholder can claim a worthless security deduction under section 165(g)(3), with regards to a CFC.

In Situation 2 of the ruling, P, a domestic corporation, owned all equity interests in FS, a foreign subsidiary. On July 1, 2003, P filed a valid Form 8832 to change FS's classification from a corporation to a disregarded entity. At the close of the day before the election, the fair market value of FS's assets, including intangible assets such as goodwill and going concern value, did not exceed its liabilities (meaning, FS's stock was worthless). Consequently, P did not receive any payment for its FS stock in the deemed liquidation. The deemed liquidation is an identifiable event that fixes P's loss, allowing a worthless security deduction under section 165(g)(3) for the 2003 tax year.

The ruling clarified that when a U.S. shareholder owns an insolvent CFC, changing the classification of the CFC to a disregarded entity can result in a section 165(g)(3) worthless stock deduction. Additionally, the creditors of the former CFC, may be entitled to a deduction for a wholly or partially worthless debt under section 166.

This ruling provides a clear pathway for U.S. shareholders of CFCs to recognize losses on worthless stock and claim appropriate deductions, thereby offering tax relief in situations where the CFC's liabilities exceed its assets.

Conclusion

Navigating the tax consequences for financially distressed CFCs is complex, particularly under the post-TCJA international tax rules. For CFCs in financial distress, understanding the relevant provisions such as section 165(g)(3) for worthless stock deductions and section 166 for bad debt deductions is crucial. Effective tax planning can help U.S. shareholders manage the tax implications of their investments in financially distressed CFCs.

This article was originally published in the AIRA Journal, Vol. 37, No. 4 in 2024.