We have made the case over the past number of years that the middle market constitutes the beating heart and soul of the American economy. As the middle market goes, so goes the U.S. economy. Based on our latest data, policymakers, investors and chief executive officers should prepare for a coming economic boom as the real economy recovers and enters expansion this year.

If there is one major takeaway from the March monthly survey, it is that middle market hiring and investment are set to accelerate: the percentages of respondents reporting plans to increase staff and make productivity-enhancing capital expenditures over the next six months posted record highs.

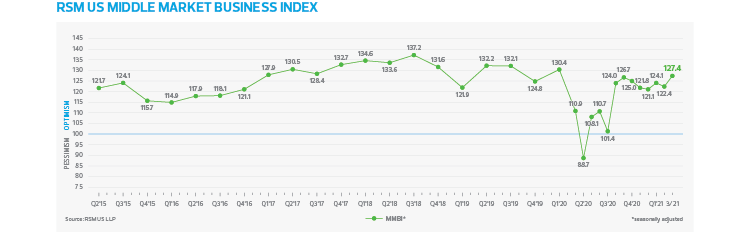

While the monthly top-line increase in the RSM Middle Market Business Index to 127.4 from 122.4 in February is impressive, the forward view is even more encouraging. Executives’ robust assessment of economic conditions, revenues, earnings, hiring, compensation and capital expenditures over the next six months underscores our position that the U.S. economy will experience a boom in 2021 that will likely unleash the strongest period of American growth since the late 1980s, and quite possibly, the post-World War II period.

If our forward-looking data is the leading indicator of the condition of the real economy that we believe it is, then we should expect substantial job gains over the remainder of 2021 with improved productivity to follow; this will help offset rising prices that survey participants note they are facing.

Beneath the top-line data, we can infer that growing confidence in economic prospects linked to rising vaccinations, and the fiscal floor put underneath the economy over the past year has bolstered middle market business confidence and is shaping expectations of changing behavior in the short term that will boost economic activity. From our vantage point, the $908 billion in fiscal aid put forward at the end of 2020 and the recent $1.9 trillion American Rescue Plan now working its way through the economy are creating conditions for a multiyear period of strong economic growth. How middle market firms manage the early phase of recovery will, in part, be characterized by constrained global supply chains and higher prices in the near term.

The path to higher growth

Perhaps the most encouraging aspect of the March survey is that a full 55% of respondents indicate that over the next six months they expect to increase productivity-enhancing capital expenditures, reflective of what we expect will be a hypercompetitive post-pandemic economy. This is the best reading in the capital spending subindex since just after the passage of the 2017 Tax Cuts and Jobs Act. Although only 35% of middle market firms surveyed are deploying more capital right now, as the economy begins to reopen, the emergence of pent-up demand by businesses to invest in their own futures, along with higher household spending, will provide the foundation of the better-than-7% pace of growth that underscores the RSM US economic forecast this year.

Along with robust growth will come some pricing pressures as the economy opens amid constrained global supply chains that were damaged during the worst of the pandemic. The MMBI prices paid subindex currently implies that prices are increasing and are expected to continue to do so in the near term. Roughly 66% of survey participants state they are paying higher prices for goods used at earlier stages of production and for intermediate goods necessary to produce finished goods, while 76% of those expect to do so six months from now.

Will these trends result in higher prices charged to middle market clients and consumers? That depends upon the ability and willingness of middle market firms to pass along higher prices paid. Our data implies that despite higher prices paid, only 43% of businesses are charging higher prices to customers, despite the increases in prices received. While 67% indicate they expect rising prices received in the near term, we wonder if those increases will materialize. In the past, rising prices have been absorbed, resulting in thinner margins, or offset through improved productivity and efficiencies, mostly due to competitive pressures. The goals of retaining market share and increasing global competitiveness have not receded and will continue to be part of the middle market narrative. As constrained supply chains are reconstituted and prices come back to earth, we would expect middle market firms to behave in a similar manner as they have over the past 30 years, and move cautiously on hiking prices.

Management of pricing issues, along with impending economic growth, will almost surely define the major narrative of the middle market over the next few years.