Following the burst of initial optimism that came with the reopening of the economy in May and early June, overall business conditions began to ease and then recede. This slowdown is showing up in a range of economic reports, including U.S. household spending and hiring, as well as alternative and near real-time data like the Harvard-Chetty database, Homebase hours-worked statistics for small and midsize businesses, mobility data and Chase’s credit card spending. All indicate that starting in mid-June, the U.S. economy began to move sideways and then down.

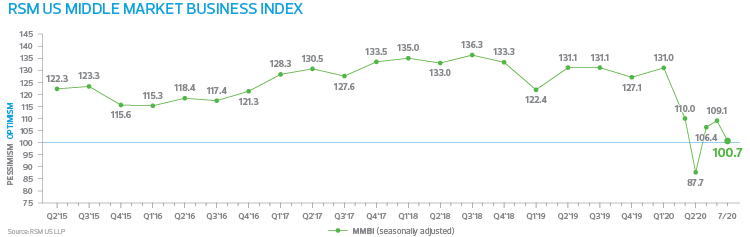

It is of little surprise that the proprietary RSM US Middle Market Business Index, a broad measure of middle market economic sentiment, eased to 100.7 in July* from 109.1 in June. This decline implies that midsize firms remain mired in recession as the pandemic has caused a series of pauses, pullbacks and shutdowns across major portions of the economy. A reading above 100 indicates that the middle market is generally expanding; below 100 suggests contraction.

Movement over the past three months inside the MMBI confirms our outlook of a swoosh-like recovery that is dependent on the progress toward the production and distribution of a vaccine, along with follow-on care, to terminate the pandemic. Traditionally, the middle market tends to lag behind the fortunes of the multinational companies that populate the public equity markets. Thus, we would not be surprised if the top-line survey tends to be somewhat volatile going forward until a vaccine is discovered.

For the most part, responses to the 10 questions that make up the index were essentially unchanged or somewhat softer, which was the primary reason for the slipping of overall middle market sentiment.

Reduced plans for hiring

Most notable were reductions in the share of respondents expecting the economy to improve (42%) and those who plan to hire additional workers (35%). The increase in the share of respondents reporting that credit was harder to obtain (41%) paralleled the most recent Federal Reserve Senior Loan Officer Opinion Survey that indicated a general tightening of credit in anticipation of rising delinquencies and defaults as business bankruptcies rise.

Beneath the headline, 29% of respondents reported gross revenues increased during the month and 46% expect an improvement over the next six months. Respondents’ views on net earnings were somewhat similar, with 31% saying that conditions had improved and 40% anticipating an improvement over the next six months. This underscores the 30% of respondents who said they had increased outlays on capital expenditures and the 39% who said they intended to do so over the next 180 days.

Only 23% of respondents indicated that they had increased hiring during the month; 35% stated they would do so six months ahead, and 38% noted that they would increase compensation over the next six months to attract talent. This clearly reflects the current dour mood among firms that populate the real economy caused by pandemic-related uncertainty.

The pricing environment modestly improved, with 52% noting higher prices paid and the same percentage noting expectations of higher prices paid going forward. Firms continue to closely manage inventories and do not plan to pass along price increases downstream. Roughly, 31% of respondents increased inventories, and 49% expect to do so early next year. Not surprisingly, 24% of survey participants increased prices and 42% expect to do so six months ahead, both basically unchanged from last month.

The full Q3 2020 RSM US Middle Market Business Index, including special questions related to business reopening considerations, will be released on August 18.

More special reports based on our proprietary MMBI research

SWIPE TO VIEW