The risks around the emerging outlook for the middle market economy include heightened summer social activity and a related second wave of infections, as well as broad fiscal and trade policy errors that could slow the pace of nascent recovery that will be underway by the end of the summer season.

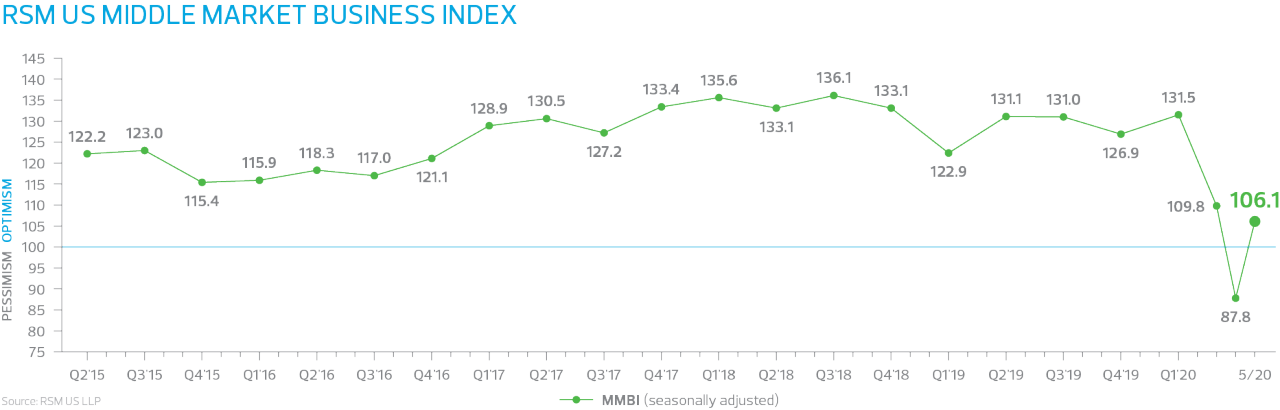

Fifty-three percent of participants in the May survey noted they expect the economy to improve over the next six months, compared with 37% currently. Over the same period, 50% of executives polled anticipate an improvement in gross revenues, while 49% expect one in net earnings. That compares with expectations of gross revenue and net earnings improvement in the current month of 28% and 29%, respectively.

Interestingly, participants also noted an expectation for higher prices paid for inputs, but they don’t expect to fully pass those costs downstream. Two things here: first, this implies risk to revenues and earnings this year, and likely reflects an assessment by midsize firms that larger upstream counterparts are not passing along their costs due to impaired consumer demand, which is likely to continue.

The projection of confidence over the economy, gross revenues and net earnings is likely associated with modest improvement in expectations around hiring and compensation. Pluralities of 40% and 39%, respectively, indicated they expect the hiring and compensation environment to improve over the next 180 days, whereas only 29% and 34% experienced upticks during May. Although caution is the best description of these labor issues currently and in the near-term, there was a noticeable bounce from historic lows associated with each measure that mirrors our forecast of tough sledding ahead in a domestic labor market. Our most optimal scenario at the end of 2020 calls for unemployment of 10%.

Among the MMBI survey findings certain to be of most interest to policymakers at the Federal Reserve—only 31% of respondents expect the borrowing environment to improve over the next six months and just 16% expect it to deteriorate. This denotes real demand for the central bank’s middle-market-focused Main Street Lending Program. In our estimation, there is a significant need for bridge and near- to medium-term financing to fund the type of revitalization, rehabilitation and innovation to the changed business landscape that will permit midsize businesses to thrive in the post-pandemic economy.

One continued area of concern that reflects Fed Chair Jerome Powell’s concern about long-term damage to the economy centers on current and expected capital expenditures. Twenty-seven percent of respondents stated it’s a good time for increasing capital outlays, which are the foundation for improving productivity, and 39% said that they would boost capital spending in the six months ahead. In the short run, productivity does not mean much. Longer term, however, it is everything. If small- and medium-sized firms pull back on productivity-enhancing investment in the post-pandemic economy, that will open the door for large firms such as Amazon to establish even more dominant positions in the economy.