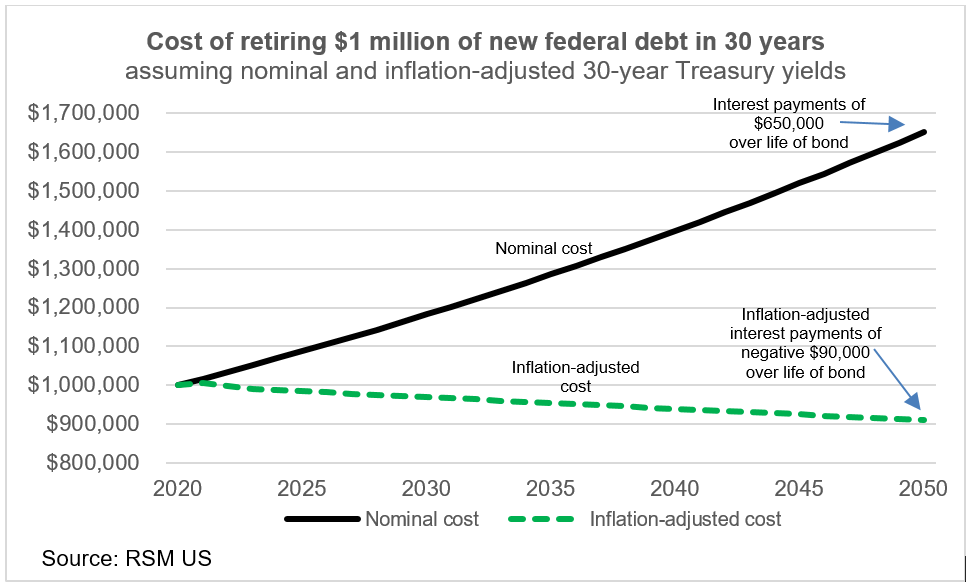

A confluence of events and policy shifts has coalesced into a unique opportunity for middle market firms to make long-term strategic investments in their firms. Interest rates, once adjusted for inflation, reside in negative terrain. This implies that firms should take advantage of those historically low borrowing costs to increase productivity-enhancing investment to prepare for the intense competition that will characterize the post-pandemic economy.

In that economy, it will be necessary for firms to pull forward investments in software, equipment and intellectual property that would have occurred over the decade into the next 12 to 24 months to prepare for the reopening of the $21.7 trillion U.S. economy and the global supply chains that support it. The potential return on investment amid real negative interest rates demands that midmarket firms act boldly and decisively to integrate advanced technologies into the production of goods and provision of services to prepare for what will be a very different economic and financial landscape than before the pandemic.

“U.S. middle market firms should act decisively to take advantage of real negative interest rates to bolster market position and create the conditions to thrive in the coming expansion.” — Brian Becker, RSM National Consulting Leader

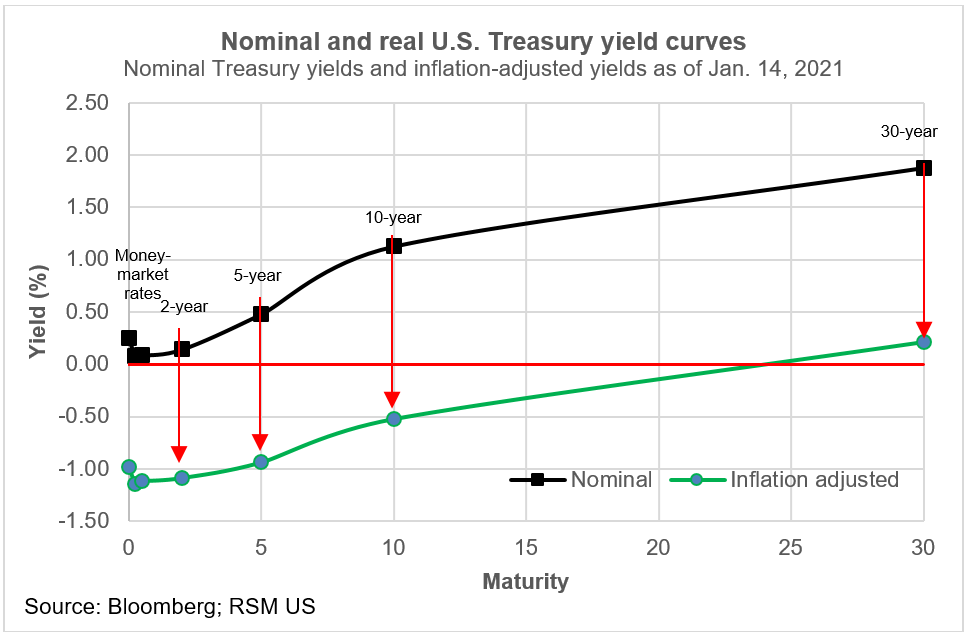

Moreover, given the shape of the yield curve and real negative interest rates well beyond the 10-year interval, an increase in spending, especially on productivity-enhancing projects, makes economic sense and will bolster the long-term prospects of the middle market firms that have the foresight to act now. Proprietary survey data taken from special questions inside the RSM US Middle Market Business Index survey over the years has consistently pointed to a deficiency in outlays on capital expenditures across the middle market.

Over the past decade, a low central bank policy rate worked in concert with reduced expectations for growth and inflation, all of which acted to pressure the entire yield curve lower. With yields out to a 10-year maturity at roughly 1% and with the inflation rate running at 1.4%, inflation-adjusted yields out to 10-year maturity turned negative.