Executive summary: Determination letters for 403(b) plans

Revenue Procedure (Rev. Proc.) 2022-40, released by the IRS on Nov. 7, 2022, allows 403(b) retirement plans to use the same individually designed retirement plan determination letter program currently used by qualified retirement plans e.g., 401(k) plans.

Rev. Proc. 2022-40

The IRS published Rev. Proc. 2022-40 along with the accompanying IRS release IR-2022-196 on Nov. 7, 2022. The Revenue Procedure permits 403(b) retirement plans, which are used by certain public schools, churches and charities, to begin using the same individually designed retirement plan determination letter program currently used by qualified retirement plans. Previously, a 403(b) plan could only have reliance that the basic terms of the plan met the 403(b) regulations if it used an IRS preapproved plan format. Complicated plans, such as plans maintained by large healthcare systems had no effective way of seeking IRS review and approval of the plan document.

Generally, an individually designed plan is a retirement plan drafted to be used by only one plan sponsor. An IRS determination letter expresses an opinion on the qualified status of the plan document. Form 5300 is the application for determination for individually designed retirement plans, Form 5307 is the application for determination for adopters of modified volume submitter or pre-approved plans and Form 5310 is the application for determination for terminating plans.

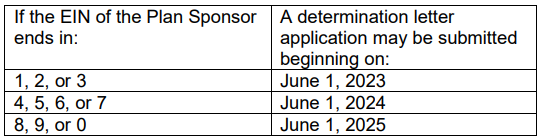

Timing of submission of determination letter applications for 403(b) plans

Beginning on or after June 1, 2023, a 403(b) plan sponsor may submit a determination letter application for newly adopted, ongoing and terminating 403(b) plans. The initial plan determination application submission dates are based on the Plan Sponsor’s EIN (see chart).

For a determination letter on plan termination (using Form 5310) a plan sponsor may submit an application anytime on or after June 1, 2023, and there is no schedule based on the EIN.

Changes for all plans

Currently, a plan sponsor can request a determination letter only if any of these apply:

- The plan has never received a favorable determination letter (an initial plan determination),

- The plan is terminating, or

- The IRS makes a special exception.

Changes to the submission and processing of all individually designed retirement plan determination letter applications include:

- A prior letter issued to a pre-approved plan adopter will not be treated as an initial plan determination – A determination letter issued to an adopter of a pre-approved retirement plan as a result of filing a Form 5307 (Application for Determination for Adopters of Modified Volume Submitter Plans) is no longer considered in determining whether a plan sponsor is eligible to submit that plan for a determination letter for an initial plan determination on a Form 5300 (Application for Determination for Employee Benefit Plan). This gives plan sponsors that have such letters an opportunity for an updated determination letter.

- Scope of review – in its review, the IRS will generally consider qualification requirements and section 403(b) requirements that are in effect, or that have been included on a Required Amendments List, on or before the last day of the second calendar year preceding the year in which the determination letter application is submitted, subject to any specified modifications in the annual Employee Plans revenue procedure that provides the administrative and procedural rules for submitting determination letter applications (currently Rev. Proc. 2022-4). For example, a plan sponsor filing a determination letter request on June, 1, 2023, would need to first review the plan against the requirements of the 2021 Required Amendment List (Notice 2021-64) and all other prior Required Amendments.

IR-2022-196 indicated that Rev. Proc. 2023-4, currently in development, will be released in the near future and will contain additional changes to procedural requirements for plan determination letter submissions, such as phasing in mandatory e-submission of determination letter requests. Forms 5300 and 5310 will also be updated to reflect these changes.