Every four years, the Securities and Exchange Commission is required by the 2010 Dodd-Frank law to modify the rules protecting investors. The original protections were put in place in 1982, but with the relentless pace of change in innovation, technology and investment options, those rules may quickly become outdated or irrelevant.

This is particularly true when it comes to the stunning growth of the family office as an investment vehicle. The concept is simple in theory: a wealthy family decides to form its own firm to look after its assets rather than rely on an outside investment adviser such as a private equity firm.

But providing safeguards has been a more difficult proposition. So in an effort to bring clarity to what constitutes a family office, the SEC in December approved measures that would streamline the definition of an accredited investor by establishing minimum asset and oversight standards.

If the measures are adopted, the accredited investor definition will be one of the tests family office investors would need to pass before investing in the private markets, including private equity, venture capital and hedge funds. The recent proposed amendments would include a number of updates but in particular, they would clearly define the role of family offices and family office clients.

Why now?

For years, the definition of a family office was unclear. Several musty pieces of legislation—the Investment Advisers Act of 1940, the Securities Act of 1933, and the Investment Company Act of 1940 – all had some legal authority over the industry.

Then in 2011, a new rule—separate from reform under Dodd-Frank—was adopted to allow family offices to provide investment advice to family members without having to register with the SEC. While this rule made it easier to establish an investment vehicle for a family, it still did not institutionalize any minimum standards for net income or wealth.

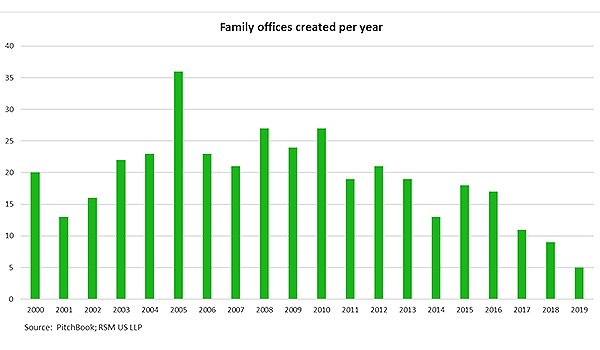

In recent years, though, pressure has been building for clarification – especially as hedge funds and private equity firms have increasingly sought to convert into a family office in a move to ease the regulatory burdens tied to operating outside money.

According to PitchBook, a research firm that compiles data on private investment and tracks family offices, there are more than 1,800 family offices around the globe, with more than 800 within the United States alone. And there are most likely more, because some family offices simply do register and are not captured in PitchBook’s data. According to a study by Campden Wealth, an independent research company, family offices manage about $4 trillion globally.