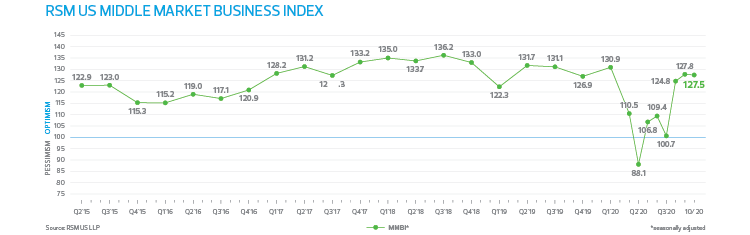

U.S. middle market business sentiment remained rock solid in October. The proprietary RSM US Middle Market Business Index eased modestly to 127.5 from 127.8 in September. For the most part, readings on the economy, revenues, net earnings and hiring remained essentially unchanged as the economy continued to emerge from the early-year recession. While it is clear that business leaders do not expect a V-shaped recovery, they do see an improvement in business conditions through the early part of 2021.

The recent intensification of COVID-19 infections in the United States and Europe has yet to dampen sentiment, but the rapid rise in cases, coupled with volatility in equity markets, suggests limited upside as the pandemic rages on. Our analysis finds that there is a strong link between the ability to contain the pandemic and the economy’s performance. Even without widespread shutdowns, consumers and businesses are likely to pull back if the pandemic intensifies, resulting in significant economic damage. For the economy to get back on track, the pandemic must be contained.

It is important to note that the survey was conducted prior to the U.S. election and the announcement that a potential Pfizer coronavirus vaccine in a large study is 90% effective, which may change the perception of current and future-looking business conditions well into next year. We would anticipate changes in middle market business sentiment in coming months. Stay tuned!

Current and future expectations around the economy did not change in October; 51% of respondents noted current improvement and 68% indicated they expected it over the next six months. For the second consecutive month, 38% of participants stated they increased hiring and 56% noted they expected to do so in the near term. Roughly 40% said they increased compensation last month, and 53% intend to do so over the next 180 days.

The percentage of executives who said revenues improved dipped to 47% from 50% previously, but 64% thought they would see an uptick by early spring. Accordingly, only 47% of participants stated that net earnings had improved, while a stout 63% expect improvement by next April. The capital expenditure outlook was modestly better, with 40% of executives stating they had increased outlays on productivity-enhancing investments and 53% indicating they will do so over the next six months.

The responses to questions pertaining to credit and borrowing signal tighter lending standards and less appetite for taking on debt, results that align with evolving trends in the Federal Reserve’s quarterly Senior Loan Officer Opinion Survey. Middle market firms were generally more upbeat on the future than about current conditions, with a slight uptick in the net percentage of respondents who said they plan to invest and hire in the next six months.

Pricing conditions eased somewhat in October, with 57% of respondents indicating an increase in prices paid and 58% noting they expect to pay more in coming months. Forty-four percent attempted to pass along price increases in the last quarter and 47% expect to do so in the near term. Finally, inventory restocking continued to modestly improve as 42% stated an increase, and 50% noted they would over the next six months.

RSM contributors

More special reports based on our proprietary MMBI research

SWIPE TO VIEW