Originally published April 9, 2020, most recently updated to reflect additional guidance announced on October 30, 2020.

The Federal Reserve on April 9 announced a $600 billion lending program to help small- and medium-sized businesses deal with the economic shock caused by the coronavirus pandemic. Additional details and terms were announced on April 30.

This new Main Street Lending Program offers five-year loans to businesses that meet specific criteria and were in good financial standing before the coronavirus crisis hit. Businesses that have taken advantage of the Small Business Administration’s Paycheck Protection Program may also take out loans under this new program. Principal payments will be deferred for two years and interest payments will be deferred for one year (unpaid interest will be capitalized) under this program..

The Department of the Treasury will provide $75 billion in equity to the lending facility, using funding from the Coronavirus Aid, Relief, and Economic Security Act (CARES Act). Businesses seeking these loans must commit to making commercially reasonable efforts to maintain payroll and retain workers. Borrowers are also required to follow compensation, stock repurchase and dividend restrictions that apply to direct loan programs under the CARES Act, with exceptions for S corporations and other tax pass-through entities.

Here’s a guide to questions businesses may have about this new program, based on information from the Federal Reserve.

Program overview

Is my business eligible for the Main Street Lending Program?

Eligible borrowers for the Main Street Lending Program are businesses that meet the following criteria:

- Have up to 15,000 employees or up to $5 billion in 2019 annual revenues (employees and revenues must be aggregated with the employees and revenues

of affiliated entities) - Must be a business established prior to March 13, 2020 and created or organized in the United States or under the laws of the United States, with significant operations in and a majority of its employees based in the United States

- Must not be an ineligible business as listed in 13 CFR 120.110 (b)‒(j), (m) ‒(s), as modified and clarified by SBA regulations for purpose of PPP on or before April 24, 2020 (including interim final rules available at 85 Fed. Reg. 20811, 85 Fed. Reg. 21747 and 85 Fed. Reg. 23450)

- May only participate in one of the Main Street facilities and must not participate in the Primary Market Corporate Credit Facility

- Must not have received specific support pursuant to the Coronavirus Economic Stabilization Act of 2020

- Must make all of the certifications and covenants required under the program

- Must make commercially reasonable efforts to retain workers and maintain payroll

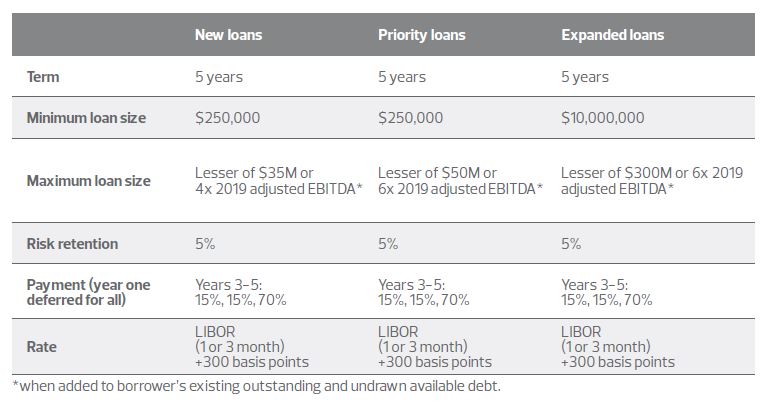

How much can I borrow?

There are three loan facilities under the Main Street Lending Program.

Loans in the Main Street New Loan Facility (MSNLF) range from a minimum $100,000 to a maximum that is the lesser of $35 million or an amount that when added to the borrowers existing outstanding and undrawn available debt does not exceed four times the borrowers 2019 adjusted EBITDA.

Loans in the Main Street Priority Loan Facility (MSPLF) range from a minimum $100,000 to a maximum that is the lesser of $50 million or an amount that when added to the borrowers existing outstanding and undrawn available debt does not exceed six times the borrowers 2019 adjusted EBITDA.

Loans in the Main Street Expanded Loan Facility (MSELF) range from a minimum of $10 million to a maximum of $300 million or an amount that when added to the borrowers existing outstanding and undrawn available debt does not exceed six times the borrowers 2019 adjusted EBITDA.

What is the rate and terms of the loan?

Loan terms are a five-year maturity at LIBOR (1 or 3 month) plus 300 basis points.

Principal payments are deferred for two years, and interest payments are deferred for one year (unpaid interest will be capitalized).

Fifteen percent of the principal will be due at the end of each of years three and four, and a balloon payment of 70% will be due at maturity at the end of the fifth year.

Prepayment is permitted without penalty.

Required certifications

In addition to certifications required by applicable statutes and regulations, the following certifications will be required from the borrower:

- The borrower must commit to refrain from repaying the principal balance of, or paying any interest on, any debt until the Main Street loan (or the upsized tranche of the loan under MSELF) is repaid in full, unless the debt or interest payment is mandatory and due

- The borrower must commit that it will not seek to cancel or reduce any of its outstanding lines of credit with the Main Street lender or any other lender

- The borrower must certify that it has reasonable basis to believe that, as of the date of the loan (or the upsizing of a loan in MSELF) and after giving effect to such loan (or upsizing), it has the ability to meet its financial obligations for at least the next 90 days and does not expect to file for bankruptcy during that time period

- The borrower must attest that it will follow compensation, stock repurchase and capital distribution restrictions that apply to direct loan programs under section 4003(c)(3)(A)(ii) of the CARES Act, except that an S corporation or other tax pass-though entity may make distributions to the extent reasonably required to cover its owners’ tax obligations in respect of the entity’s earnings. The CARES Act conditions, which are summarized below, apply through the duration of the loan and for 12 months after the date on which the loan is no longer outstanding

- May not repurchase an equity security that listed on a national securities exchange of the business or any parent company of the business, except to the extent required under a contractual obligation that was in effect on the date of enactment of the CARES Act (March 27, 2020).

- May not pay dividends or make other capital distributions with respect to the common stock of the business.

- Must comply with limitations on compensation under section 4004 of the CARES Act, which are summarized below:

- Officers or employees with total compensation over $425,000 in calendar year 2019 shall not receive total compensation in excess of what was received by the officer or employee in calendar year 2019. Severance pay or other benefits received upon termination shall not exceed twice the total compensation received by the officer or employee in calendar year 2019.

- Officers or employees with total compensation over $3 million in calendar year 2019 shall not receive total compensation over $3 million and 50% of the excess over $3 million of what was received in calendar year 2019.

- The borrower will be required to certify that it is eligible to participate in the program, including in light of the conflicts of interest prohibition in section 4019(b) of the CARES Act.

It is important to note that the Federal Reserve Bank’s special purpose vehicle (SPV) for this lending program will stop purchasing participations in eligible loans on Sept. 30, 2020, unless the Board of Governors of the Federal Reserve System and the Treasury Department extend the facility. The Federal Reserve Bank will continue to fund the SPV after that date, until the SPV’s underlying assets mature or are sold.