Kevin Warsh, in his first meeting as Fed chair, signaled that the central bank would emphasize price stability.

Key takeaways

The recent upward pressure on prices will prompt the central bank to consider a rate hike in the near term.

That rate hike could come as soon as September, depending on the direction of inflation before then.

After much speculation, executives and investors last month got their first glimpse of how Kevin Warsh would approach leading the Federal Reserve, as the central bank held rates steady and adopted a decidedly hawkish tone on inflation.

By holding its policy rate between 3.5% and 3.75% at the Federal Open Market Committee meeting on June 17, the Fed signaled that it would emphasize price stability over maximum employment.

The data backs that stance: The Fed’s preferred, inflation metric, the personal consumption expenditures index, rose to 4.12% in May, as we had forecast.

The upward pressure on prices will prompt the central bank to consider a rate hike in the near term to keep inflation expectations in check and restore price stability over the next few years.

The recent inflation data strongly suggests that Warsh’s honeymoon ended before it began.

We predict the FOMC meeting on July 28−29 will be a status quo event—meaning it will hold rates steady. But the September meeting will be a “live” policy meeting, and a rate hike could be on the table.

Because of the recent surge in inflation, the FOMC removed the easing bias from its policy statement, which is now a mere four paragraphs. Gone is this sentence: “In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks.”

While the statement removes near-term guidance, our reading of the Fed’s shift is anything but neutral. Unless the inflation data eases in the near term, a rate hike may be on the way.

Warsh’s radical reworking of the policy statement, including the removal of forward guidance, signals a change in the direction of the Fed under his leadership.

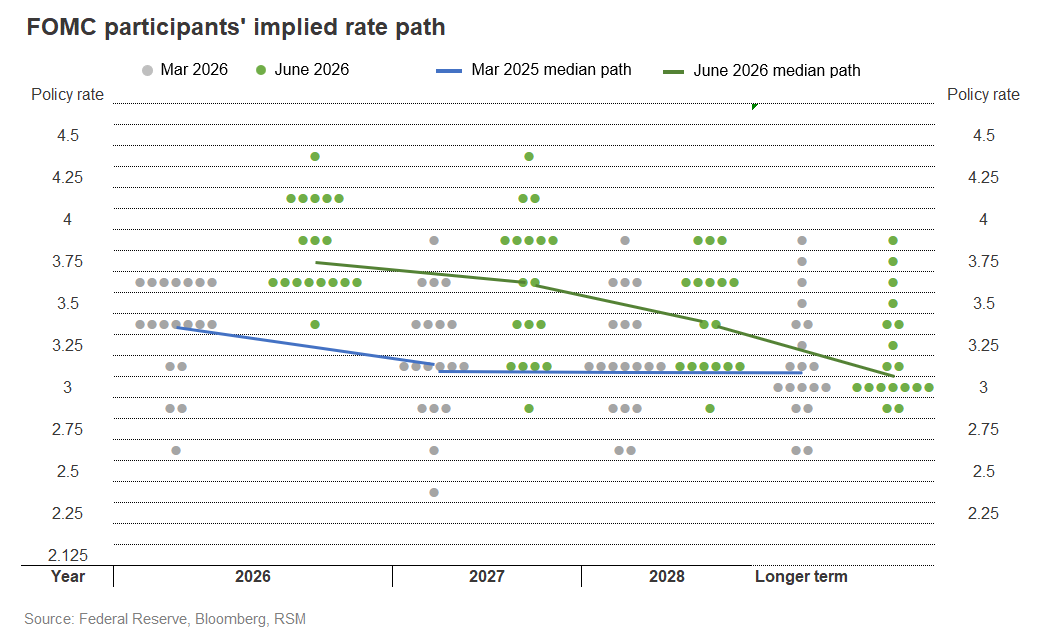

But the fact that a dot plot, or interest rate forecast, was produced, with Warsh demurring, suggests that forward guidance is not dead at the Fed and that the new chairman does not have the support of the majority to make some of the changes he wants.

His decision not to offer an interest rate forecast is an example of Warsh’s stated interest in making deliberations less public and letting the Fed’s actions speak for themselves.

The overriding message from Warsh’s first meeting was the central bank’s focus on containing inflation. The changes in the statement, along with dot plot submissions indicating that nine of the 18 members favor a rate hike this year, suggest that the FOMC is coalescing around a focus on price stability.

Fed officials see a median rate of 3.8% at the end of 2026 and 3.6% in 2027. The policy statement reaffirmed an ample reserves policy for the banking system—meaning no near-term policy changes—and the committee unanimously supported that decision.

Every key inflation measure—the PCE, core PCE, consumer price index, core CPI, producer price index and core PPI—stands above the current federal funds rate and well above the Fed’s 2% target.

With inflation floating above that target for more than five years, there is a growing risk that the public will reset inflation expectations higher. In our view, that is why the policy statement, along with the Summary of Economic Projections and the dot plot interest rate forecast, points to a hawkish hold.

The economic and supply shocks of the past several years, combined with the capital expenditure boom, strongly imply that looking through the current supply shock—which is pushing inflation higher— would pose a real risk to price stability.

Summary of Economic Projections

The SEP revised its projection for 2026 growth in gross domestic product down to 2.2% from 2.4%, while keeping its 2027 forecast at 2.3% and raising its 2028 forecast to 2.2% from 2.1%. The long-run growth projection remained at 2%.

The unemployment rate forecast dropped to 4.3% from 4.4% for 2026 and remained at 4.3% for 2027 and 4.2% for 2028. The long-run forecast held steady at 4.2%.

The major changes in the SEP were in the inflation forecast. The Fed lifted its PCE inflation forecast to 3.6% from 2.7% for 2026, raised it to 2.3% from 2.2% for 2027, and kept it at 2% for 2028. The long-term PCE estimate remained at 2%.

The forecast for core PCE inflation rose to 3.3% from 2.7% for this year, to 2.5% from 2.2% for 2027, and to 2.1% from 2% for 2028.

The projected federal funds rate for 2026 now stands at 3.8% versus 3.4% previously, and at 3.6% for 2027 and 3.4% for 2028. The long-run federal funds rate remains unchanged at 3.1%.

The takeaway

The FOMC’s June policy decision leaned hawkish because of the recent surge in inflation, which has created the possibility of a near-term rate hike.

While we do not expect the July meeting to be “live” with a policy change on the table, we anticipate that by September the committee will know far more about risks around the inflation outlook, putting a rate hike in play at that time.