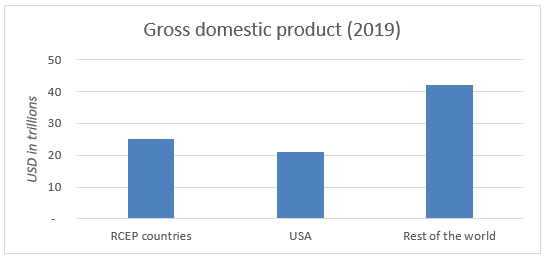

In mid-November, China signed a regional trade agreement—the Regional Comprehensive Economic Partnership (RCEP)—with 14 other Asia-Pacific countries. Touted as the world’s largest regional free trade agreement, it includes countries that make up 30% of the world’s gross domestic product. But it does not include the United States, even though some of the countries that signed the pact—for example, Japan, Australia, Singapore and South Korea—are strong American allies.

The partnership is one of the latest developments in the ongoing battle for economic dominance between China and the United States. News of the RCEP also comes as President-elect Joe Biden is preparing to take office, with a platform that we expect to include a more multilateral approach to China than we have seen under President Donald Trump.

All of this prompts a question: How can businesses navigate the current geopolitical environment? Businesses want certainty and for their investments to be protected, but they need to be aware of the uncertainty that may come with investing or operating in China.

While the economic benefit from the RCEP remains to be seen, it will provide a platform for trade and cooperation between China and its Asian counterparts, bolstering its growth and dominance. The Trans-Pacific Partnership, or TPP, which the United States pulled out of in 2017, was created in part as a counterweight to China’s growth. It is widely expected that the Biden administration will rejoin the TPP to reassert America’s role. But it remains to be seen if the new administration will have the political capital to win over critics of the deal, including some on the left who object to certain labor-related provisions in the TPP, and some on the right who have a more hawkish view on China trade.