The first two articles in this issue of The Real Economy explore the Federal Reserve's dilemma of taming inflation while maintaining full employment. They are from a series examining the overriding monetary and fiscal policy challenges in today's economy. Read part 2 here.

In the year ahead, the economy and financial markets will be influenced by how the Federal Reserve strikes a balance between its dual mandates of full employment and price stability.

With inflation at its highest point in decades, we think the central bank will move to normalize its monetary policy by first winding down its asset purchases and then raising interest rates—all without undermining the recovery.

The extent to which the Fed manages to bring down inflation and strike that balance will largely determine the lifespan of its flexible average inflation targeting policy or set the stage for an opportunistic increase in the 2% target to 3% in the coming years.

As the normalization in rates takes place this year, we do not expect steep increases like those that took place under Paul Volcker, even if inflation proves stubborn this year and next.

This is why the market has priced in three rate hikes this year, with a 90% possibility of a fourth. But even that may end up fewer given the likely appointment of three Fed members who are almost certain to lean toward the full employment side of the Fed’s dual mandate.

Traditionally, fiscal and monetary authorities have moved to counter inflationary pressures through aggressive tax, monetary and regulatory policies. That means tax and interest rate increases, as well as policies that result in a better allocation of capital that discourages bubbles, whether they are in housing or financial markets.

Given the use of the Fed’s balance sheet as a policy tool over the past two decades, it is likely that the central bank will choose to permit a runoff of its balance sheet this year.

Between 2017 and 2019, the Fed let its balance sheet fall by roughly $50 billion per month. In our estimation, Fed officials will most likely allow that to reach $100 billion once it begins, which will probably happen after the Federal Open Market Committee policy decision in September.

Tax hikes, though, seem unlikely for now, and changing incentives around housing and financial investment will take time to work.

It all puts more pressure on the Fed to counter inflation by raising interest rates and by reining in speculative investment through public persuasion, known as open-mouth operations.

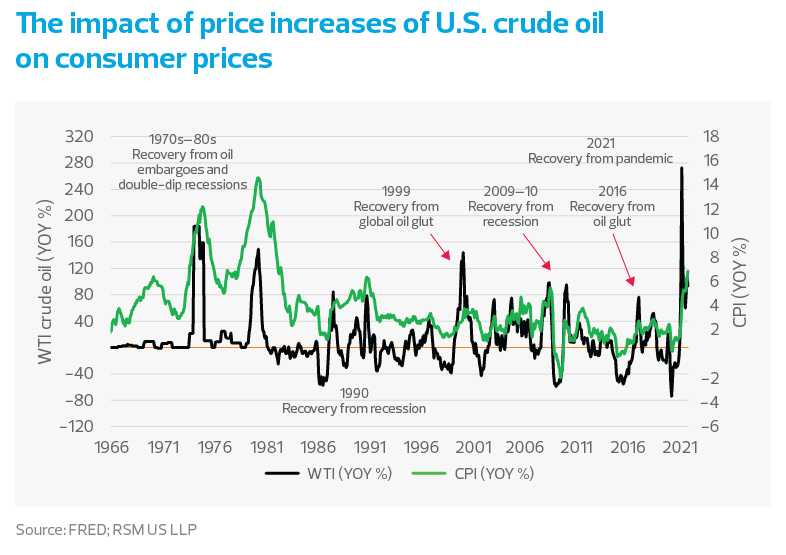

With inflation surging, there have already been calls for emergency price controls used to combat shortages during World War II and then again, in response to the OPEC oil embargoes in the 1970s.

While for some, selective price controls would be preferable to Fed rate hikes that have the potential of derailing the recovery, we would disagree.

The imposition of price controls under current conditions would be a grave error that would only provide an illusion of short-term stabilization. The more likely outcome of price controls would be medium-term distortions and longer-term dislocation across the economy.